Learn what a credit score is, how to check your score, factors that increase or decrease it, and the benefits of maintaining a good score. Beginner-friendly guide.

Credit Score Explained for Beginners: Everything You Need to Know

Imagine you are a fresh college graduate who has just started earning money. One day, you decide to buy a car, rent an apartment, or apply for a credit card. Before approving your request, banks and financial institutions want to know one thing:

Can this person be trusted to repay borrowed money?

This is where your credit score becomes important.

A credit score acts like a financial report card. Just as your academic grades help employers understand your educational performance, your credit score helps lenders understand your financial behavior.

In this guide, we’ll explain credit scores in the simplest way possible.

1. What Is a Credit Score?

Credit score is a numerical rating that represents how trustworthy you are when it comes to borrowing and repaying money.

Think of it as a score that summarizes your financial discipline.

The score is usually calculated based on your borrowing and repayment history. Different countries may use different scoring systems, but generally, a higher score means lower risk for lenders.

Simple Example

Let’s say there are two people:

Rahul

- Pays all loan EMIs on time

- Pays credit card bills before the due date

- Has never missed a payment

Amit

- Frequently misses payments

- Pays bills late

- Has defaulted on a loan

Who would a bank trust more?

Obviously, Rahul.

As a result, Rahul will have a higher credit score than Amit.

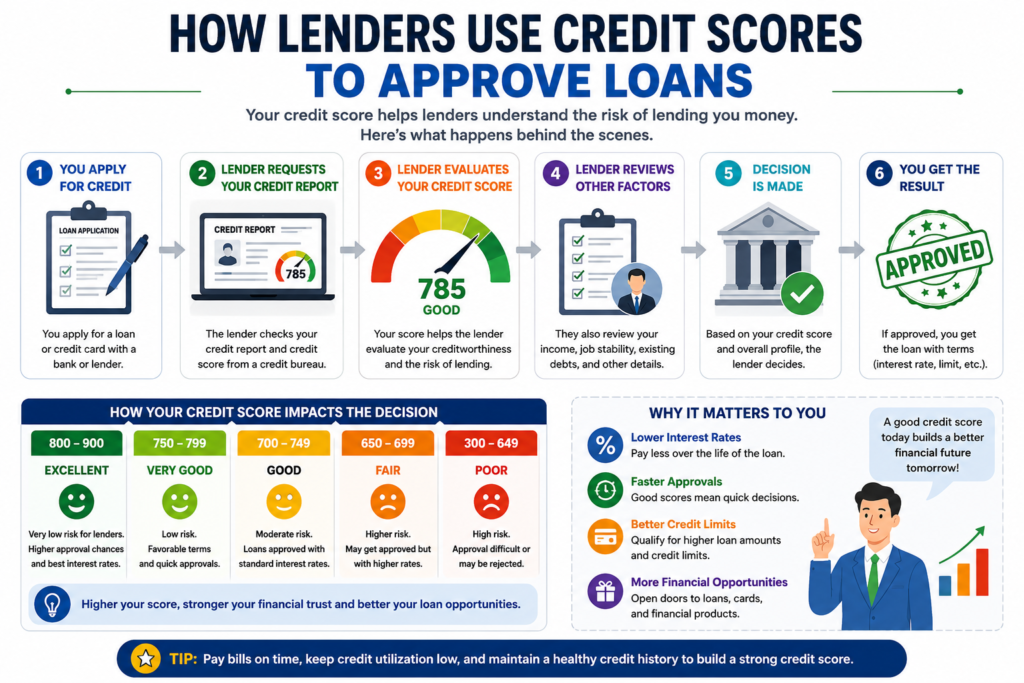

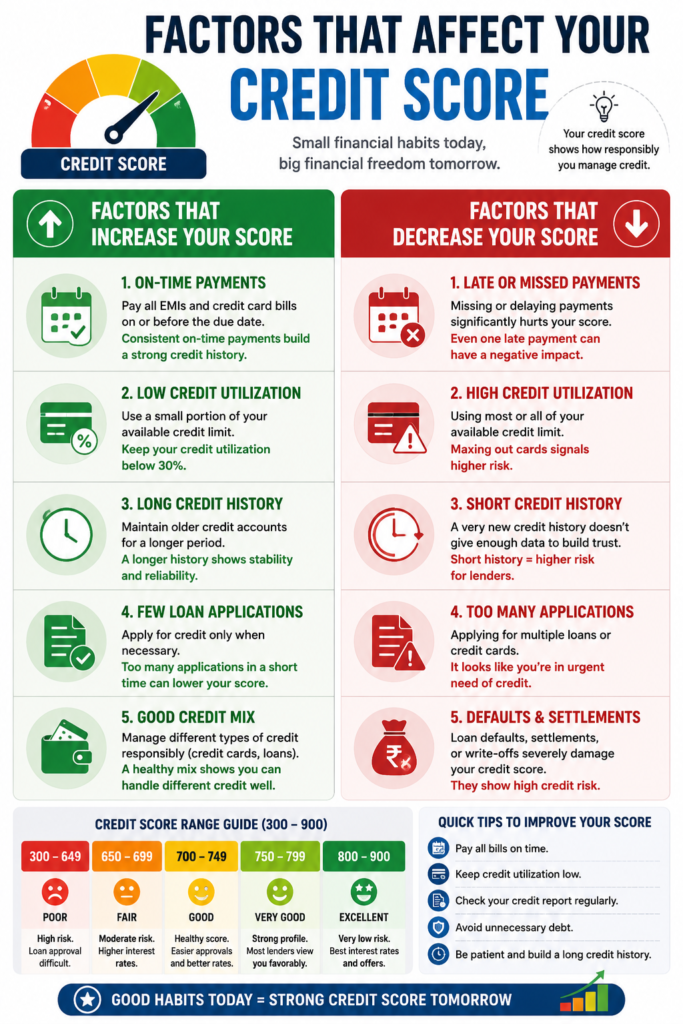

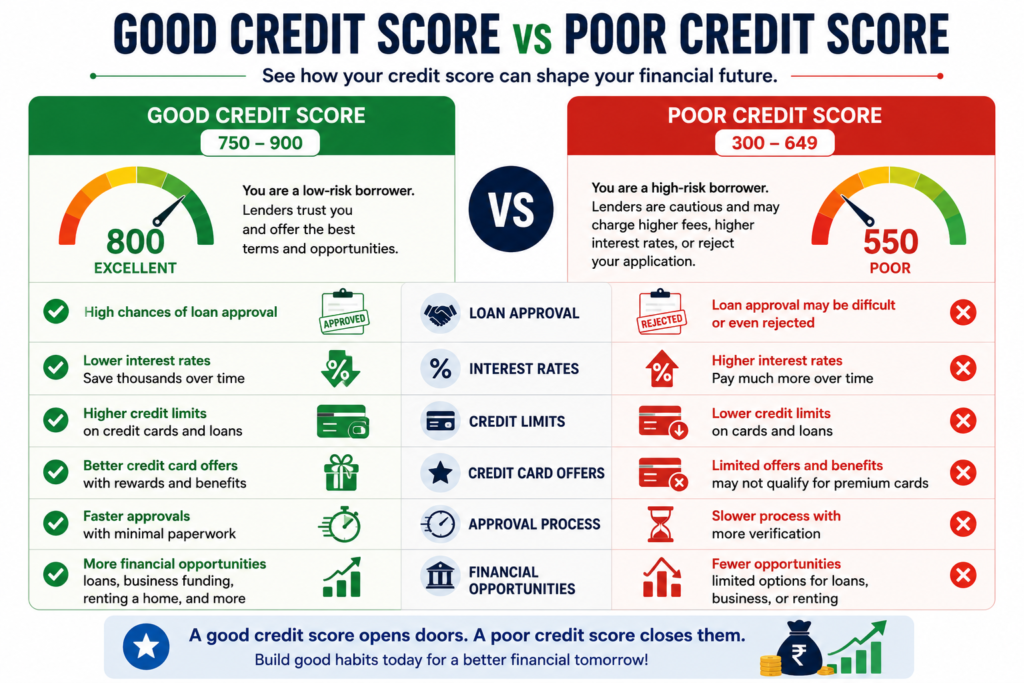

Understanding Credit Score Ranges

While the exact scoring range can vary slightly between countries and credit bureaus, many credit scoring systems use a scale similar to 300 to 900.

Here’s a simple way to understand what different score ranges generally mean:

| Credit Score Range | Rating | What It Means |

|---|---|---|

| 800 – 900 | Excellent | Lenders see you as a very low-risk borrower. You are more likely to get loans approved quickly and may qualify for the best interest rates. |

| 750 – 799 | Very Good | Indicates strong financial discipline and a good repayment history. Most lenders will view you favorably. |

| 700 – 749 | Good | Considered a healthy score. Loan and credit card approvals are generally easier, although you may not always receive the best rates. |

| 650 – 699 | Fair | Shows moderate creditworthiness. You may still get approved for credit, but lenders may be more cautious. |

| 300 – 649 | Poor | Indicates higher lending risk. Loan approvals may become difficult, and interest rates may be significantly higher. |

What Score Should You Aim For?

If you’re just starting your financial journey, a good target is:

✅ 700+ = Good Score

✅ 750+ = Very Good Score

✅ 800+ = Excellent Score

A score above 750 is often considered ideal because it can improve your chances of loan approval and help you qualify for better interest rates and credit card offers.

Tip for Fresh Graduates: Don’t worry if you don’t have a credit score yet. Everyone starts with no credit history. By using credit responsibly and paying bills on time, you can gradually build a strong score over the years.

Why Does a Credit Score Exist?

Banks, lenders, and financial institutions lend money to millions of people.

They cannot personally interview everyone to determine whether they are financially responsible.

It helps them make faster decisions by answering questions such as:

- Does this person repay borrowed money on time?

- Has this person missed payments before?

- How risky is it to lend money to this individual?

- How likely is the borrower to repay the loan?

The higher the score, the more confidence lenders have in you.

How Can You Find the Credit Score of a Person?

Checking Your Own Credit Score

You can check your own score through:

- Credit bureaus

- Banking applications

- Financial service platforms

- Credit report websites

Typically, you need:

- Full name

- Date of birth

- PAN card or national identification number

- Registered mobile number

After verification, you can access your credit report and score.

Can You Check Someone Else’s Credit Score?

Generally, No.

A person’s credit score is private financial information.

You cannot legally access another person’s credit score without their permission.

Only authorized institutions such as banks, lenders, and approved financial organizations can view someone’s credit report when the individual gives consent.

Example

If your friend asks:

“Can you tell me my score?”

You can guide them on how to check it themselves.

However, you cannot simply look it up without authorization.

Which Factors Affect a Credit Score?

Your score constantly changes based on your financial behavior.

Some habits increase your score, while others decrease it.

Let’s understand each factor.

1. Payment History

This is one of the most important factors.

It tracks whether you pay:

- Loan EMIs

- Credit card bills

- Other borrowed amounts

Increases Credit Score

✔ Paying every bill on time

✔ Never missing due dates

Decreases Credit Score

✘ Late payments

✘ Missed EMIs

✘ Loan defaults

2. Credit Utilization

Credit utilization means how much of your available credit limit you are using.

Example

Credit card limit: ₹100,000

Amount spent: ₹20,000

Credit utilization = 20%

Lower utilization is generally considered healthier.

Increases Credit Score

✔ Using a small portion of your available credit

✔ Keeping utilization below reasonable levels

Decreases Credit Score

✘ Frequently maxing out credit cards

✘ Using nearly all available credit

3. Length of Credit History

This refers to how long you have been using credit products.

Example

Person A:

- Using a credit card for 8 years

Person B:

- Opened first credit card 2 months ago

Person A generally has a stronger credit history.

Increases Credit Score

✔ Maintaining older accounts responsibly

Decreases Credit Score

✘ Having a very short credit history

4. Number of Loan Applications

Every time you apply for a loan or credit card, lenders may review your credit profile.

Too many applications within a short period can signal financial stress.

Increases Credit Score

✔ Applying only when necessary

Decreases Credit Score

✘ Applying for multiple loans simultaneously

✘ Frequent credit card applications

5. Types of Credit Used

Using different credit products responsibly can demonstrate financial maturity.

Examples include:

- Credit cards

- Education loans

- Auto loans

- Home loans

Increases Score

✔ Managing different credit accounts responsibly

Decreases Score

✘ Mismanaging multiple loans

✔ Habits That Help Increase Your Credit Score

If you’re starting your financial journey, follow these simple habits:

Pay Bills on Time

Set reminders or automatic payments.

Keep Credit Card Usage Low

Avoid spending your entire credit limit.

Avoid Unnecessary Loans

Borrow only when necessary.

Monitor Your Credit Report

Check periodically for errors or suspicious activity.

Maintain Older Credit Accounts

Long-term responsible usage strengthens your profile.

✘ Habits That Can Reduce Your Credit Score

Avoid these common mistakes:

- Missing EMI payments

- Late credit card payments

- Maxing out credit cards

- Applying for many loans at once

- Defaulting on loans

- Ignoring credit report errors

Even a few bad financial decisions can affect your score for years.

Benefits of Having a Good Credit Score

A good score offers several advantages.

Think of it as having a strong reputation in the financial world.

1. Easier Loan Approval

Banks are more likely to approve your:

- Home loan

- Car loan

- Personal loan

- Education loan

2. Lower Interest Rates

Lenders often reward low-risk borrowers with better interest rates.

Example

Person A:

- Score: Excellent

- Interest rate: Lower

Person B:

- Score: Poor

- Interest rate: Higher

Over time, this difference can save thousands or even lakhs of rupees.

3. Better Credit Card Offers

People with good scores may qualify for:

- Higher credit limits

- Premium credit cards

- Cashback rewards

- Travel benefits

4. Faster Approval Process

Since lenders trust applicants with strong scores, approvals may be quicker.

5. Greater Financial Flexibility

A strong score gives you more borrowing options when you need money for:

- Education

- Business

- Emergencies

- Major purchases

6. Increased Financial Trustworthiness

A good score sends a message:

“This person manages money responsibly.”

This reputation can be valuable throughout your financial life.

Real-Life Example

Imagine two recent college graduates applying for a car loan.

Priya

- Pays bills on time

- Uses credit responsibly

- Never misses payments

Score: High

Result:

- Loan approved quickly

- Lower interest rate

Rohan

- Misses payments

- Has multiple loan defaults

- Uses all available credit

Score: Low

Result:

- Loan approval becomes difficult

- Higher interest rate

This shows how financial habits today affect opportunities tomorrow.

Conclusion

A credit score is one of the most important numbers in your financial life. It reflects how responsibly you manage borrowed money and helps lenders decide whether to trust you.

For someone just beginning their financial journey, the best strategy is simple:

- Pay all bills on time

- Borrow responsibly

- Keep credit card usage under control

- Avoid unnecessary debt

- Monitor your credit report regularly

A good score can make loans easier to obtain, reduce borrowing costs, and open the door to better financial opportunities throughout your life.